🐙 Su$tainable Mobility: The Founder's Guide to Hacking Debt

Vol 54

This bi-weekly newsletter aims to separate the signal from the noise for making money in sustainable transportation: Electrification, mode shift, active and public transit, and mobility aggregation, across both people and goods movement.

I had a great couple of days at the NREL Industry Growth Forum earlier this week. I’ll be at several climate events for LA Tech Week (June 5-11); let me know which ones you’ll be attending.

This week’s Deep Dive is The Founder’s Guide to Hacking Debt. Alternative title: Please don’t use $300M in venture capital to buy commodity e-scooters.

Submit startups & ideas for the newsletter here.

🌱STARTUP WATCH: Sustainable mobility startups (pre-seed or seed) to keep an eye on

Battery Streak (California, USA): Lithium-ion batteries w/nanostructured titanium niobium oxide anode (instead of graphite) for ultra-fast charging

Blyncsy (Utah, USA): AI software to improve the safety and efficiency of traffic networks

Fin (United Kingdom): Zero-emissions last-mile delivery network

Jawnt (Pennsylvania, USA): Fintech to help employers offer transit options to their employees

Magpie Aviation (California, USA): Mid-flight tow aircraft for long-range zero-emissions aviation

Mini Mines (India): Li-ion battery recycling

MoveEV (Massachusetts, USA): Fleet electrification planning software for enterprises

Roev (Australia): Pickup truck EV conversions

Tandem (New Jersey, USA): Attachable hybrids for heavy-duty trucking

Telo Trucks (California, USA): Manufacturer of small electric pickup trucks

💰FUNDING: Capital raises from startups previously featured in Startup Watch

Alt Mobility (Vol 26) raised a pre-seed round (undisclosed amount) from Piper Serica Angel Fund *

Dovetail Electric Aviation (Vol 41) won a $3M (Australian $) research grant from the Australian federal government, as well as an investment from Regional Express *

Fluxart (Vol 45) raised a £100K grant from TechX Clean Energy Accelerator *

Infyos (Vol 45) raised a pre-seed round (undisclosed amount) from Nucleus Capital and Pale Blue Dot

Gage Zero (Vol 51) raised an undisclosed amount in private equity from ARC Financial

Reminder: The startup data set is open, for free. If you’re a subscriber interested in accessing the Airtable with all the raw data on ~400 companies, please let me know.

📰QUICK HITS: Notable news from the last two weeks

👩🏽⚖️Government, Policies & Cities

🤧 The US Federal government approved NYC’s congestion pricing plan! Expect last-minute appeals from folks in the NY area, but the dam is now broken. For more context on the importance of this, read Vol 49: Is New York City on the Cusp of Making Mobility History?.

🚕 Speaking of, Washington, D.C. is looking at congestion pricing for ridehail. With NYC’s momentum, lots of North American cities will start looking at curb management solutions and more modest congestion pricing solutions.

📦 Following the first-in-the-nation zero-emissions delivery zone from LACI and Santa Monica, Portland is adopting the concept as well. Curb management solutions continue to be essential for zero-emissions delivery zones.

🏪 NYC is experimenting with microhubs for last-mile delivery. Alongside curb management, micro-hubs help make zero-emissions delivery zones feasible.

🅿️ US House Rep. Robert Garcia will introduce a bill to ban parking minimums near public transit. The sooner we kill parking minimums, the better.

🚫 Lisbon temporarily banned cars from driving through the city center. While done to facilitate some major construction projects, this one might become permanent.

🇧🇪 In Belgium, all employees now earn a tax credit for biking to work (link in French). Another example of Belgium’s rapid embrace of sustainable mobility after years of being a European laggard.

🇫🇷 France has budgeted 2 billion EUR to boost bike usage. Paris has become a case study on the pivot to sustainable mobility, but converting smaller cities will be a huge challenge.

😢 Culver City, California caved to pressure and scrapped its protected bike lane program. Not all the news this issue is positive!

🤔 Clark County is moving forward with plans to expand its Vegas Loop with The Boring Company by another 25 miles. Wait until they discover subways.

🇩🇪 Germany created a national mass transit subscription. Public transport all across Germany at a flat rate of €49 per month sets a standard for other regions.

💪🏾 California approved a ban on sales of diesel heavy-duty and medium-duty trucks as of 2036. This is historic and bold. Given the healthy regulatory rivalry between California and the EU, look for an eventual EU response.

🚂 California passed a first-in-the-nation rule on zero-emissions rail cars. Another example of California setting the tone for the nation and, at times, the world.

🚲 California is moving closer to a statewide e-bike rebate program. The devil is in the details on making these programs equitable and efficient.

💸 The Texas House unanimously approved a bill to charge EV owners a $200 per year registration fee versus an average of $71 for gasoline-powered cars. In the end, the most equitable solution is a vehicle miles traveled (VMT) fee for all vehicles, with weight and tailpipe emissions being factored in.

🔬Markets & Research

🏇 California reached its EV car goals 2 years early. What once seemed nearly impossible difficult turned out to be more than achievable.

☺️ New research shows that we are back to moving around as much as pre-COVID, but with less diversity in our trips. The heterogeneity of physical encounters in cities drives economic productivity, so it’s concerning that our urban trips are in a rut.

🏭 Corporates & Later Stage

↘️ Lyft laid off one quarter of its staff. Not out of the woods yet.

🔩 GM is killing the Chevrolet Bolt. This is understandable given that the Bolt doesn’t leverage the lower-cost Ultium platform. Still, it’s another example of where GM looks inconsistent in the EV rollout.

🕐 Mercedes is pushing off its short-term electrification goal by one year. A culprit here is the disastrous situation for foreign automakers in a rapidly electrifying China.

🆓 Tesla is quietly trying to get some of its customers to give up free Supercharger access for life. Alas, those who cost Tesla the most in free charging are going to be the least likely to redeem this offer.

🔥 BP avoided a shareholder revolt on climate action, but problems are still brewing. The path forward for oil & gas companies is nothing if not contentious.

🐣 Startups & Early Stage

🎉 Blink charging network acquired EV-as-an-amenity startup Envoy (Disclosure: I’m affiliated with LACI Impact Fund I, which invested in Envoy). Congrats to the Envoy team for successfully scaling a novel approach to EV car sharing.

😿 European scooter operator Tier is exploring a sale. The micromobility winter isn’t over yet.

📉 Lordstown Motors is on the brink of bankruptcy, again. Freed from Lordstown Motors, Foxconn will be able to focus more on the Lordstown factory as their white-label EV manufacturing hub in North America. For more see, Vol 47: The Fox(conn) is Guarding the Henhouse.

🌊 The first Fisker Ocean delivery took place, thanks to manufacturing by Magna. An example of contract manufacturing success in the EV space. For more, see Vol 4 on the re-emergence of contract manufacturing.

DEEP DIVE: The Founder’s Guide to Hacking Debt

It’s easy for founders to get the impression that their job is to fuel growth via venture capital funding. After all, how often does TechCrunch cover someone securing a debt facility? Even in this newsletter, the database is generally tracking venture and grant funding, but not most debt.

The job of startup leadership is to:

First: determine company and founder objectives around economics and control

And then: Determine the best financing mix of self-funded, grant, equity (including, but not limited to, venture capital), and debt.

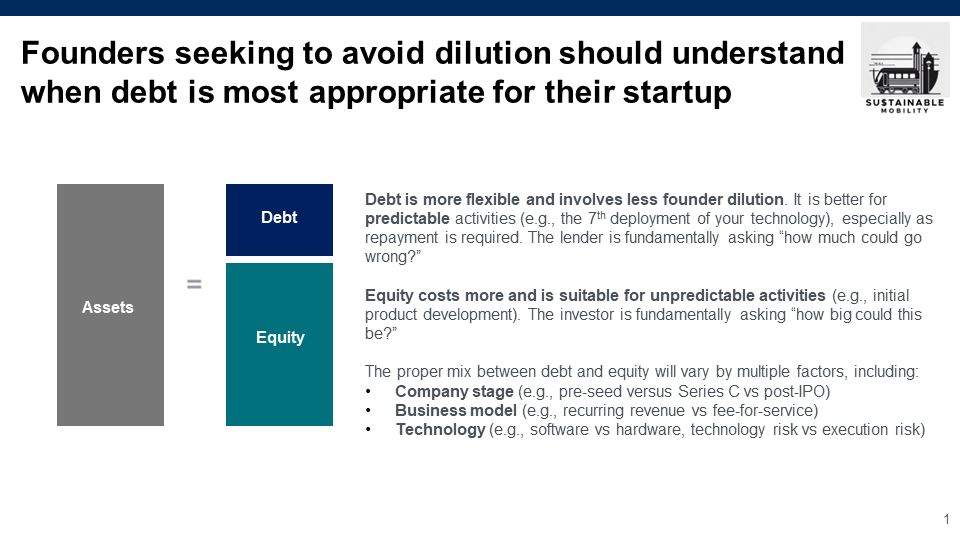

In their haste to scale companies, many founders ignore the debt angle until too late and find themselves unnecessarily diluted. Early-stage founders can and should understand their debt options, even at the seed-stage.

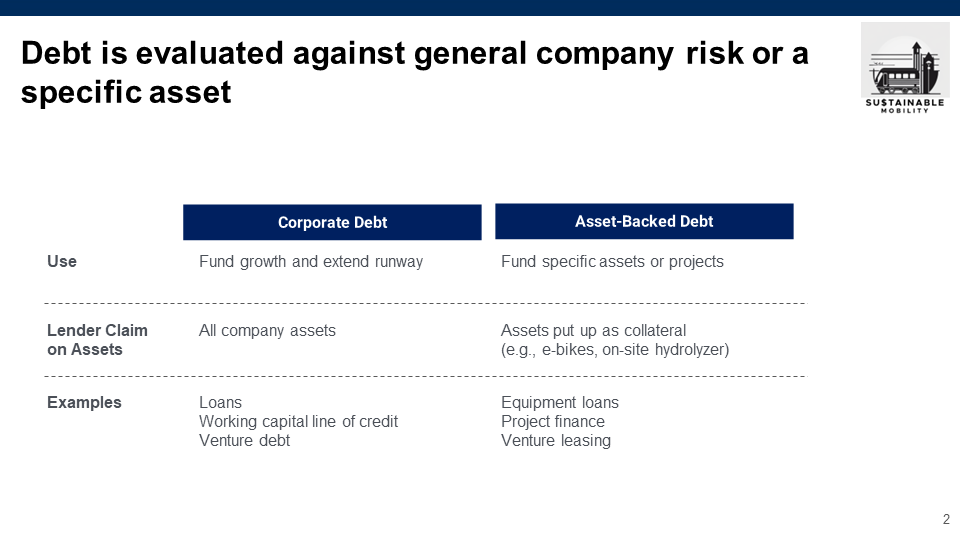

However, it’s a mistake to approach debt lenders in the same way you would approach a venture capitalist. While a VC fundamentally cares about “how big could this be?”, a debt lender is agonizing over every little thing that could go wrong. The “up and to the right” hockey stick growth projection chart that’s powerful with VCs can put off the more conservative debt lender.

They’re also keenly focused on understanding whether they are underwriting the entirety of the company or a specific asset or project. Be as specific as possible about what your capital needs are and whether they’re for the organization or a specific cash flow.

In particular, founders should be aware of climate-specific lending instruments available even at the earlier stages.

Securing earlier-stage debt won’t garner you a press article, but in the long term it could mean avoiding a point or two of dilution on a $500M valuation. And who doesn’t love getting to keep an additional $5 to $10M?

* Several of these raises happened in Q4 2022 and Q1 2023. Such are the perils of scouting companies before they show up in Crunchbase much later.

Alex, This was such a rich and helpful resource. As a founder currently raising our seed, this helped me get a sense of the funders we already know as well as others in the space. Thank you !

Great read as always !!! Please cover India’s ONDC initiative and promise it holds in revolutionising mobility as a service