🚨Su$tainable Mobility: The Next Cold War is Already Here

Vol 41

This bi-weekly newsletter aims to separate the signal from the noise for making money in sustainable transportation: Electrification, mode shift, active and public transit, and mobility aggregation, across both people and goods movement.

The Deep Dive this issue: The next Cold War is already here. The global market for the battery economy and chips is breaking down into trade fiefdoms. Those who don’t acknowledge this code red will be left behind in the EV transition.

If you’ll be in LA next week, consider joining this happy hour on Wednesday, Nov 16 on the sidelines of Comotion.

QUICK HITS: Notable news from the last 2 weeks

🛩 In Amsterdam and over a dozen other cities in the world, climate activists are blocking private jets from taking off. Private jets are the new fur coat; the criticism will likely abate once private jet operators go electric.

🌉 San Francisco asked voters via proposition whether to allow cars on JFK Drive and 60% said no. Elected city officials generally waver on car moderation measures, so look to other American cities (where allowed) to go directly to the voters on such measures.

🚦Berkeley may ban “right turn on red” to protect pedestrians and cyclists. How the tables have turned. If you’ve seen Annie Hall, you may remember that the original practice of right turn on red originated in California and spread elsewhere in the US during the 1970s energy crisis.

🔁 In Los Angeles, the hyperloop demonstration prototype has been dismantled. Hyperloop is having a rough go of it.

🇫🇷 France is requiring that parking lots be covered in solar. If you’re going to have large parking lots, you might as well have them serve as energy and charging hubs.

🇸🇦 Saudi Arabia is launching its own EV manufacturer, in partnership with Foxconn. See volume 4 for more context on Foxconn’s long game. Other large emerging markets will no doubt be watching, as will large fleet operators.

💀In a letter to its clients, the hedge fund Elliott sounds the alarm about hyperinflation and potential “societal collapse.” An alleged copy of the letter here notes the incredible supply chain pressure to scale renewables (and presumably batteries); more along those lines in the Deep Dive below.

🚁 United Airlines and Archer announced their eVTOL plans for Newark airport; Abu Dhabi Airport announced its eVTOL plans as well. For the record, I’ll continue to take the Newark AirTrain to public transit.

🛫 Fuel-saving “blended wing body” airplane designs may be ready for takeoff. Look for this to come to cargo planes via customer pull from the likes of Amazon and FedEx before it comes to passenger planes.

♻️ Lime announced a battery 2nd life program and Audi teamed up with Redwood Materials to let customers recycle consumer electronics at Audi dealers. Both are great examples of how the battery chain for consumer electronics is linked with the battery for transportation applications. That said, the Audi model doesn’t seem convenient for the customer.

🔋The UK startup battery manufacturer Britishvolt is still alive…barely. This one appears to be a victim of the painful decline of British industry.

🌊 National governments are uniting against seabed mining. Their position is that much more scientific research is needed to understand environmental impacts before mining EV battery inputs on the ocean floor.

🍳Elon Musk bought Twitter; GM, Sellantis, and VW all paused their ad spending on the platform (among many others). It’s hard to see how major spenders will want to advertise on Twitter until Musk can provide consistent and clear messaging.

🚗 Faraday Future is looking messier and messier, as is van maker Arrival. Launching a car company is very, very hard.

🚙 Lucid is suing Texas to allow it to bypass dealers. In the long term, US dealership protection laws are doomed, but in the short term, there’s room for lots of legal wrangling.

5️⃣ Renault is splitting into 5 different companies under 1 holding, in part to cope with the EV transition. This seems clever in theory, but complex in reality. In the end, much of Renault may end up a Geely subsidiary, alongside Volvo Cars, Lotus, etc.

💧Hydrogen fuel cells may finally be coming of age, but perhaps only in long-distance heavy-duty trucking for surface transport applications. The article is a good primer on the overall state of hydrogen in surface transportation.

🏇 Lyft laid off 13% of its workforce, lost a California ballot initiative it sponsored, and its stock sank to an all-time low. If Lyft folds, Uber finally wins monopoly status in the US ridehail market.

🚲 Sequoia Capital invests in Chinese e-bike manufacturer Aveton at a $590M valuation. The US doesn’t yet have the domestic supply chain to create such companies…currently.

🛴 A research study in Atlanta claims that e-kickscooters can potentially save an average of 17% in travel time for people in the US. Ultimately, shared e-kickscooters will become an integrated part of public transit offerings.

STARTUP WATCH: Sustainable mobility startups (generally pre-seed or seed) to keep an eye on

🛩 Dovetail Electric Aviation (Australia): Electric retrofit solution for small aircraft

🚢 eyeGauge (France): Digital twin for maritime emissions reduction

📲 Go To-U (California, USA): Consumer EV charging app

👨🏾💻 Haylon Technologies (Illinois, USA): Battery management software (BMS) focused on reducing li-ion waste

🛣 Kilows (Washington, USA): Batteries + shipping containers = EV charging for highways

🔌 Luma (Sweden): V1G/V2G for EV virtual power plants

🚠 Swyft Cities (California, USA): Gondola-like public transport system

FUNDING: Capital raises from startups previously featured in Startup Watch

Lift Ocean (Vol 2) raised a $2.3M seed round from Yinson Holdings and others (Note: raise was announced in April 2022, not updated until now in Airtable database as raise not captured in Crunchbase)

Aviant (Vol 4) raised a $740k round from Innovation Norway and others (Note: raise was announced in Oct 2021, not updated until now in Airtable database as raise not captured in Crunchbase)

Electric Era (Vol 30) raised a $4M seed round from Proeza Ventures, Blackhorn Venture, REMUS Capital, and Liquid 2 Ventures

(Reminder: The complete startup dataset is free for subscribers. If you’re a subscriber interested in accessing the Airtable with all the raw data of the 250+ companies, please let me know below.)

DEEP DIVE: The next Cold War is already here

The Cold War ended on Dec 26, 1991, when the USSR was dissolved, leaving the US as the sole superpower. That same year also marked the end of COMECON, the Eastern Bloc’s trade group. Its Western Bloc equivalent, COCOM (Coordinating Committee on Multilateral Export Controls) wound down in 1994 after almost 50 years of controlling exports of sensitive goods to Soviet-aligned states.

The end of the Cold War marked the beginning of a period of economic growth and the supposed triumph of liberal democracies with a global free trade agenda. A decade later, for example, China joined the World Trade Organization.

Today, many expect that China’s (re) emergence as a global superpower will lead to conflict and potential war with the US, the declining superpower (see Thucydides Trap for more info). That would likely spell the end of the institutions created by the US post World War II such as the World Bank, the IMF, and the WTO.

Actions around the world over the last few years suggest that the world’s great powers (the US, China, and the EU) have both consciously and accidentally laid the groundwork for a trade-focused cold war, with the stakes including the battery and chip economy that underpins EVs. In short, the next cold war is already here; call it Risk: The EV Trade Edition.

In the last few months, we’ve seen the following:

The US Inflation Reduction Act tied EV tax credits to domestic sourcing, resulting in vocal protests from trade allies like Korea and the EU, as well as China.

European carmaker Stellantis announced it was dissolving one of its two struggling joint ventures in China. CEO Carlos Tavares claimed the “interference of the political agenda has been increasing by the day”, and that “there is growing political interference in the way we do business as a western company in China.”

The US imposed harsh export controls aimed at stopping China from becoming a full-stack semiconductor superpower. This comes amidst a global semiconductor shortage, hampering auto production.

France and Germany may have agreed to work on a plan to protect European EV manufacturers from Chinese and American competition.

Mineral-rich countries are actively studying whether to set up OPEC-like cartels.

EVs and the energy transition aren’t the cause of this trade war, but rather one of the most visible and urgent symptoms of it. Countries recognize that national security is interwoven with technology leadership in batteries and chips, and the inevitable supply chain choke points as we scale EVs globally. So while the US and the EU are desperately trying to build up their own battery supply chains, China and others are weighing whether to cut off adversaries’ access to supply chain components.

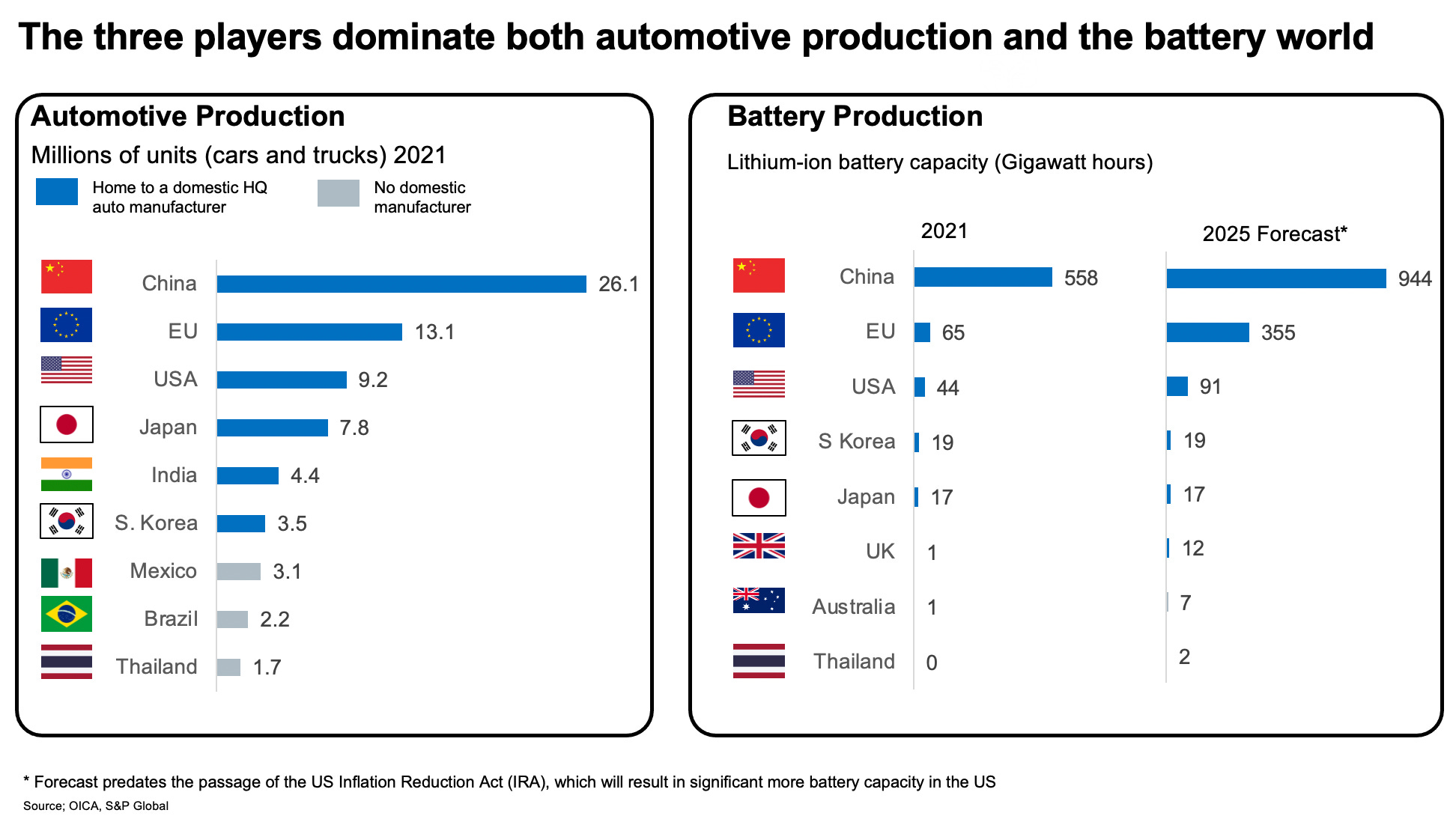

Let’s start our game with three core players, each starting from a very different point. China is ahead of the other two players in the EV trade war but has many headwinds. The US, the declining hegemon, still has a lot of firepower, both metaphorical and literal. And finally, there’s the wildcard player: the EU. It may choose to play this game as a solo player or as a partner with one of the other two. China and the US don’t appear to have that option with each other.

In this game, it’s paramount to be prepared for one of the other players to cut you off. Even in a world of truly global free trade, there would have been inevitable supply chain choke points with our collective desire to grow EV sales, such as augmenting mining capacity, building battery recycling capacity, and so on. But now, everyone’s turning their back on global free trade for political reasons.

At the same time, none of the major players can pull off this alone, which means the rest of the world becomes ground zero for rewritten trade rules and development agreements. South Korea and Japan are both important participants, with advanced capabilities in batteries and chips, but neither with enough heft to write their own rules. Similarly, Taiwan plays an increasingly uncomfortable role as a chipmaker of choice, caught between Chinese and US interests.

A more complicated same story plays out on the mining side, with batteries today reliant on lithium, nickel, and cobalt. Expect this country list to change over time as countries realize the opportunity and necessity of taking advantage of resource abundance in their own territories.

In the end, mid to large-size economies like India and Brazil will get some say in who they pick for their alliances, as will those blessed and cursed with important mineral deposits like Congo. But dozens of countries will have no choice at all.

We’re in the early stages of this trade war. The major players need to double down on domestic production (of batteries, chips, and cars), strong R&D, ironclad mineral supply agreements, and scalable battery recycling capabilities. Otherwise, you’ll just end up a piece on someone else’s game board when they decide to put you on their trade sanctions list.