🎉 The 100th Issue Celebration 🎊

Vol 100

This newsletter aims to separate the signal from the noise for investment in all things sustainable transportation: Electrification, mode shift, active and public transit, and mobility aggregation, across both people and goods movement.

So here we are: the 100th issue. And for this Deep Dive, I’ve opted not to focus on the dramatic political shifts in the last few weeks and their impact on sustainable mobility. The TLDR is that sustainable mobility involves interactions between assets (e.g., zero-emissions cars, zero-emissions plane charging infrastructure) and behaviors (e.g., using a mapping app to realize the bus gets you faster there than your car). At the asset level, the Trump administration is as powerless as anyone else against the ongoing decrease in battery costs; every long-term projection shows EVs being cheaper (and higher performing) than internal combustion engine cars. EVs are mature enough globally that trying to slow their progress will only result in economic and environmental damage in the US. More to come in a subsequent Deep Dive.

So to celebrate issue 100, today’s Deep Dive analyzes which sustainable mobility startups got funded in 2024. Armed with dry powder, these startups should give us hope for what progress can be made, especially in the face of political headwinds in the US.

🌱STARTUP WATCH: Sustainable mobility startups (pre-seed or seed) to keep an eye on

Estes Energy (California, USA): Chemistry-agnostic battery platform with a US-supply chain

evPower.ai (Israel): Operator of a bidirectional EV charging network

Flitedeck (Germany): A digital cockpit for bicyclists (notably, the company has been funded so far via an OnlyFans account. Link safe for work)

HiveLink (France): Interactive displays for public transit

OpenRoad (California, USA): Hardware and software platform for high-speed EV charging

Pleevi (Belgium): Charging management software for large charging facilities

Tubular Network (Texas): Interconnected system of tubes that can autonomously transport packages between buildings

Vivant Cycleworks (California): Emerging manufacturer of e-cargo bikes

🌱STARTUP WATCH: Sustainable mobility startups (pre-seed or seed) to keep an eye on

FlexCharging (Vol 27) was acquired by Accurant’s FlexEnergi unit. This is the 13th exit in the dataset

Presto (formerly ChargePass, Vol 48) raised a $15M Seed round from Union Square Ventures, Congruent Ventures, Powerhouse Ventures, and Jetstream

ENAPI (Vol 78) raised a $7.5M Seed round from Voyager Ventures, Project A, Seedcamp, and helloworld

Dreamfly Innovations (Vol 88) raised a $1.4M Seed round from Avaana Capital and SunICON Ventures

As a reminder, the startup data set is free (for now) to subscribers. If you’re a subscriber interested in accessing the Airtable with how these startups raised $2.5 billion in follow-on funding, please let me know.

📰QUICK HITS: Notable news from the last two weeks

👩🏽⚖️Government, Policies & Cities

👍 In NYC, congestion pricing continues to deliver good results across vehicle traffic, subway and bus ridership, foot traffic for retailers, and now has support of 60% of New Yorkers. Whether the potential new Federal Transit Administration secretary kills it is anyone’s guess.

👌🏾In California, Caltrain’s commuter rail notched a 41% increase in passenger volumes after switching to electric. In another nice bonus, the electricity costs are about 15% less than what Caltrain had expected.

💲At the state level, California’s high-speed rail program faces a $6.5B funding shortfall. Trump said he may investigate the project.

🚄 China has unveiled a prototype of the world’s fastest train, hitting an operational speed of 400 km (~250 miles) per hour. Meanwhile, Acela only hits 240 km (150 miles) per hour.

🪦At the US federal level, the transportation policy changes in the last two weeks have been astounding: The US withdrew (again) from the Paris Climate Accord. President Trump ordered the elimination of the federal “electric vehicle (EV) mandate”. While there is no federal EV mandate, it’s likely to mean that federal fuel economy standards get watered down or eliminated. The new DOT secretary made his first attack on any agency work relating to climate change. And trade allies Canada and Mexico were threatened with what the Wall Street Journal called “The Dumbest Trade War in History.” Those tariffs are currently on hold, but if they become real, expect chaos in the EV industry.

🔬Markets & Research

💧The European aviation sector’s decarbonization roadmap got its first update since 2021, with a dramatic reduction in the deployment of hydrogen as a fuel for planes. Sustainable aviation fuel and hybrid electric for short-haul appear to be the winners.

🤖 The Driverless Digest did a great overview of Waymo vs Uber. Author Harry predicts that Waymo ultimately offloads network operations to Uber or someone else. See a hint of this with Uber’s announcement to add Waymo to the mix in Austin.

🏭 Corporates & Later Stage

🦾 Speaking of Waymo, they’ve added 10 new cities to their 2025 plan. They’re just testing there…for now.

☯️ Tesla’s earnings call for Q4 and the full year 2024 was exactly what everyone expected. Bulls heard Elon Musk’s plan to create the AI behemoth for the physical world, from self-driving to intelligent robots. Bears heard an executive team unable to acknowledge why a 70% deterioration in profitability last quarter was of any concern.

🐂 For the Tesla bulls: In addition to Musk suggesting a $30 trillion valuation, he committed to launching the company’s robotaxi network in Austin by June. It’s also conceivable that Musk redirects federal policy to prioritize Tesla’s lower-grade autonomy technology over Waymo’s more safety-minded approach.

🧸 For the Tesla bears: Since the earnings call, Tesla’s January sales vs the prior year were down by 11% in China, 63% in France, almost 60% in Germany, and by 10% in the US. Tesla’s very light Model Y refresh only underscores how long in the tooth the vehicle is.

🐢 Tesla expects to finally reach mass production of its Semi Truck by the end of this year. That’s another calendar year for Volvo Group and Daimler to build their lead in EV semis.

♟️Uber announced great earnings and activist investor Bill Ackman took a $2B stake in the company. Ackman is known for bitter courtroom battles, but he came out of the gate heaping praise on Uber’s current management.

💦 Renault’s CEO, testifying before a French parliamentary committee, noted “there is no market for hydrogen vehicles.” The testimony is linked to Renault’s plan to shut down its joint venture that makes hydrogen vans.

😨 Nissan canceled its planned tie-up with Honda, balking at the idea of becoming a Honda subsidiary. This ups the chances that Nissan eventually ends up a subsidiary of Foxconn; see the Deep Dive “The Fox(conn) is guarding the Henhouse” for more.

📫 GM’s robotaxi unit Cruise is laying off half its staff. The remainder of the staff will be folded into GM operations.

🐣 Startups & Early Stage

👋 Norway’s Freyr abandoned its plans to build a $2.6B battery plant in Georgia. As global trade barriers increase, expect disruption in manufacturing plans.

🛩️ ZeroAvia’s electric plane moved one step closer to full FAA certification. One step closer to short-haul aviation being a battery affair…

🚢 Corvus Energy is helping build the first world’s fully electric offshore vessel. Many inland waterway vessels (e.g., ferries) are going electric, but this is taking batteries out into the open seas.

🚄 Brightline West launched a $2.5B bond sale to finance part of its LA to Vegas high-speed rail plan. It aims for standard one-way ticket price of $119, but the opening has been pushed to after the LA Olympics.

🏴☠️ Beleaguered electric truck maker Nikola is expected to imminently undertake bankruptcy proceedings. It’s unlikely that someone will buy the remaining assets.

Know someone who should be following this space? Share this issue with them:

DEEP DIVE: WHAT GOT FUNDED IN 2024 AND WHY

Rather than focus on potential doom and gloom, this Deep Dive analyzes the companies in the Startup Watch that received fresh capital in 2024. Armed with dry powder, these founders should give us hope about what can be accomplished for sustainable mobility in 2025 even amidst American and global headwinds.

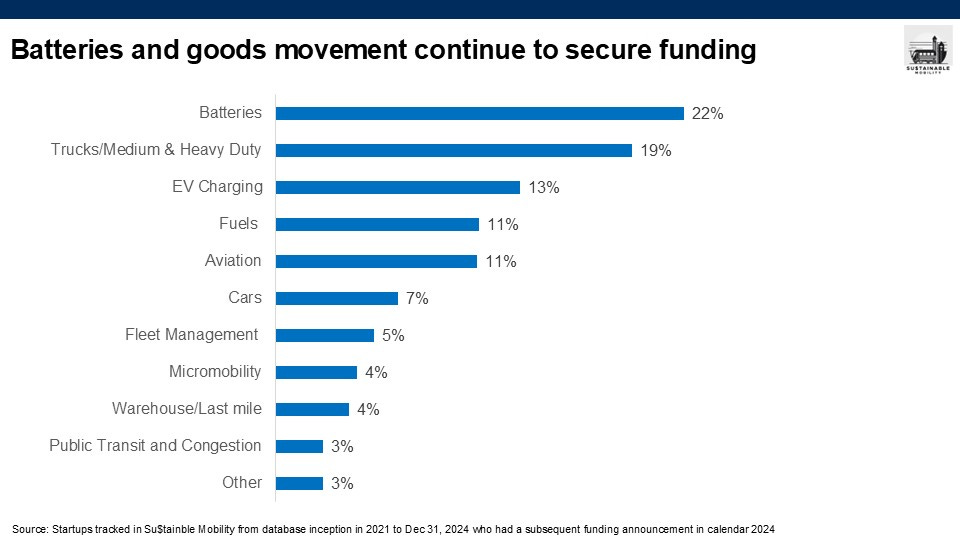

Of the 788 companies in the Startup Watch database from inception in 2021 to the end of 2024, 104 announced a subsequent funding event in 2024 and 4 had an exit. Of the funding events, 10 didn’t disclose the amount raised. The remaining 94 startups raised $761M, for an average of $8M per company.

Ten startups nabbed over one-third of that capital and, notably, only two of those could be described as software plays. The rest all involve some sort of physical product.

Geography-wise, startups based in California secured 34% of the funding, with the UK (11%), Germany (11%), Massachusetts (10%), and New York (7%) rounding out the top players. East Africa, led by Kenya, continues to be an emerging hotbed of activity.

In terms of sub-sectors, batteries, trucking, and EV charging account for over half the dollars, which looks similar to 2023 fundraising.

So what does that tell us about this year?

🔋 The nearshoring of the battery economy in the West is imperative and garners bipartisan support in both North America and Europe. Getting both the institutionalization of battery R&D and manufacturing will be a herculean challenge, but tensions with China don’t look like they will cool anytime soon. This continues to be a huge opportunity in everything from using AI to identify sustainable mining sites in North America to building the next Redwood Materials for battery recycling.

🚛 On the heavy-duty side, there’s still a meaningful opportunity for new entrants, given how much the entire ecosystem needs to change as Volvo and Daimler (and BYD) scale EV trucks- think everything from the massive charger challenges to labor issues integrating autonomy.

🚙 The electrification of cars is no longer a venture business. A decade ago you could raise billions for a car startup like Lucid. No more. Future deal activity in this space is more likely to be M&A, as outsiders like Foxconn ponder buying companies like Nissan or as legacy players consolidate in an attempt to counter the dominance of China’s EV players.

✈️ On the aviation front, the US government can’t let Boeing fail, but it probably wouldn’t be opposed to a new domestic player joining the scene. And it’s more than likely that a new player would leapfrog Boeing and its suppliers on the powertrain front. Take Anduril, which is out for a $2.5B raise and has deep connections to the Trump administration. Given Anduril’s ties to eVTOL player Archer, it doesn’t take too many product cycles to see how Anduril could start making Boeing sweat, first on the defense side, and then potentially on civil aviation.

🚢 Sustainable maritime, which is about half of the “other” category, is still under the radar. While large portions of the maritime decarbonization will be PE or project finance deals, this continues to be an area ripe for startup-led disruption.

2025 is likely to be a tough year. But in an environment where the US federal government is turning its back on all things climate, it’s an opportunity for startup founders and investors to refocus on fundamentals: scaling a startup often comes down to having a superior costs and performance versus legacy companies.

Here’s to the next 100 issues…and thanks for being along for the journey thus far…

Thanks for publishing these, Alex! One question: in your seed section you always list the location of companies you mention, but in subsequent mentions you link to where they were previously mentioned instead. Would you mind including the location with those links to previous mentions? I’m always on the lookout for Colorado companies - there aren’t too many, so needing to click through for each one is a bit clunky :)