🪓 Su$tainable Mobility: Not all Layoffs are Created Equal

Vol 34

This bi-weekly newsletter aims to separate the signal from the noise for making money in sustainable transportation: Electrification, mode shift, active and public transit, and mobility aggregation, across both people and goods movement.

This week we have a Deep Dive on trying to make sense of the layoffs in sustainable mobility.

I’ll be speaking with StartOut about where climate change meets the LGBTQ+ community on Sept 15, 2022 as part of their 3rd annual Equity Summit. Join us!

🇧🇪 Brussels’ mode share went from 55% private car in 2019 to 45% in 2022. Biking is exploding, proving that mid-size cities can have a huge climate impact if they can find the political will to build biking infrastructure.

🐟 Seattle is again debating whether to close Pike Place Market to cars. Bonus points to whoever can convince small businesses of the many case studies showing how restricting parking either keeps shopper foot traffic steady or improves it.

🇩🇪 Germany’s nearly free public transport is alleviating road congestion. I’ll probably do a deep dive on this topic at a certain point, as I think free public transit isn’t the slam dunk it appears at first glance. But I like this execution in Germany.

🔥 This essay shows how city policy in developed markets can inadvertently make cities hotter, not cooler. Our addiction to land use policies like building more roads and parking are hurting our climate ambitions. Better to turn that energy towards parking maximums, urban tree canopies, and cool pavement technologies.

➡️ A new data set reconfirms that one of the biggest impediments to transportation decarbonization is the slow turnover of our vehicle stock. This is why I get excited about EV retrofits for certain vehicle classes (e.g., some commercial vehicles), e-bikes and mobility aggregators, the tipping capability of curb management, fleet platforms like DoorDash, etc.

👋🏼 Bolt has bolted in multiple US cities. All is not well in shared mobility land.

💰Uber got to cash flow positive for the first time. Time will tell when it can reach cash flow positive and positive net income on a sustained basis. In the interim, Uber will likely sell many of its minority equity investments.

🚁 American Airlines has ordered 250 eVTOL air taxis. Still a lot of open questions about whether noise pollution on eVTOLs will be manageable and in what use cases.

🚛 Truck manufacturer Volvo Group announced plans for a large-scale battery plant in Sweden. Volvo continues to build a lead on heavy-duty electric truck deliveries while Tesla’s Electric Semi may or not begin deliveries by the end of 2023.

🔋Stellantis outsold Tesla in battery electric vehicles (BEVs) in Europe in the first half of 2022. Stellantis clocked 105k units, behind VW’s 116k and well ahead of Tesla’s 78k. That’s a big difference versus the American market, where Tesla’s lead is still strong.

🇺🇸 The Inflation Reduction Act (a modified Build Back Better bill) is still very much on the table. If it passes, I’ll do a deep dive on it. Winners include the US EV supply chain; losers include the e-bike industry.

🚛 Nikola purchased Romeo Power for $144M, 11% of Romeo’s initial SPAC value. The SPAC mania hangover is real.

🔋Panasonic is planning a $4B battery plant in Kansas. Panasonic’s existing North American manufacturing in Nevada had been joined at the hip with Tesla. The Kansas City location, an almost 11-hour drive to Tesla’s Texas factory, suggests that Panasonic is getting serious about serving other OEMs in North America.

📦 Amazon started deliveries with Rivian vans in many cities. Stellantis electric van deliveries to Amazon begin next year, so Rivian needs to scale production ASAP.

🛩 Everyone’s mad at Taylor Swift for her private jet’s CO2 consumption. While the global impact of such behavior is negligible, it’s good to see broader public engagement in the climate debate. Negative points to Taylor’s team for thinking that it would help her case to clarify that her jet is often borrowed by lots of other celebs. Luckily, short-haul aviation is about to tip towards electric in the same way that passenger cars started tipping towards electric a few years ago.

STARTUP WATCH: Sustainable mobility startups (generally pre-seed or seed) to keep an eye on

AIO Motors (California, USA): 1 passenger, 4-wheeled micromobility EV

Adapt (California, USA): Carbon calculation for fleet operators

BatX (India): Battery recycling

Radian BiKube (Texas, USA): Radar to prevent car or truck collisions with cyclists

Urban Radar (France): Urban mobility software and data marketplace

FUNDING: Capital raises from startups previously featured in Startup Watch

As announced last issue, I am making the startup data set open, for free. If you’re a subscriber interested in accessing the Airtable with all the raw data of the 200+ companies, please let me know below.

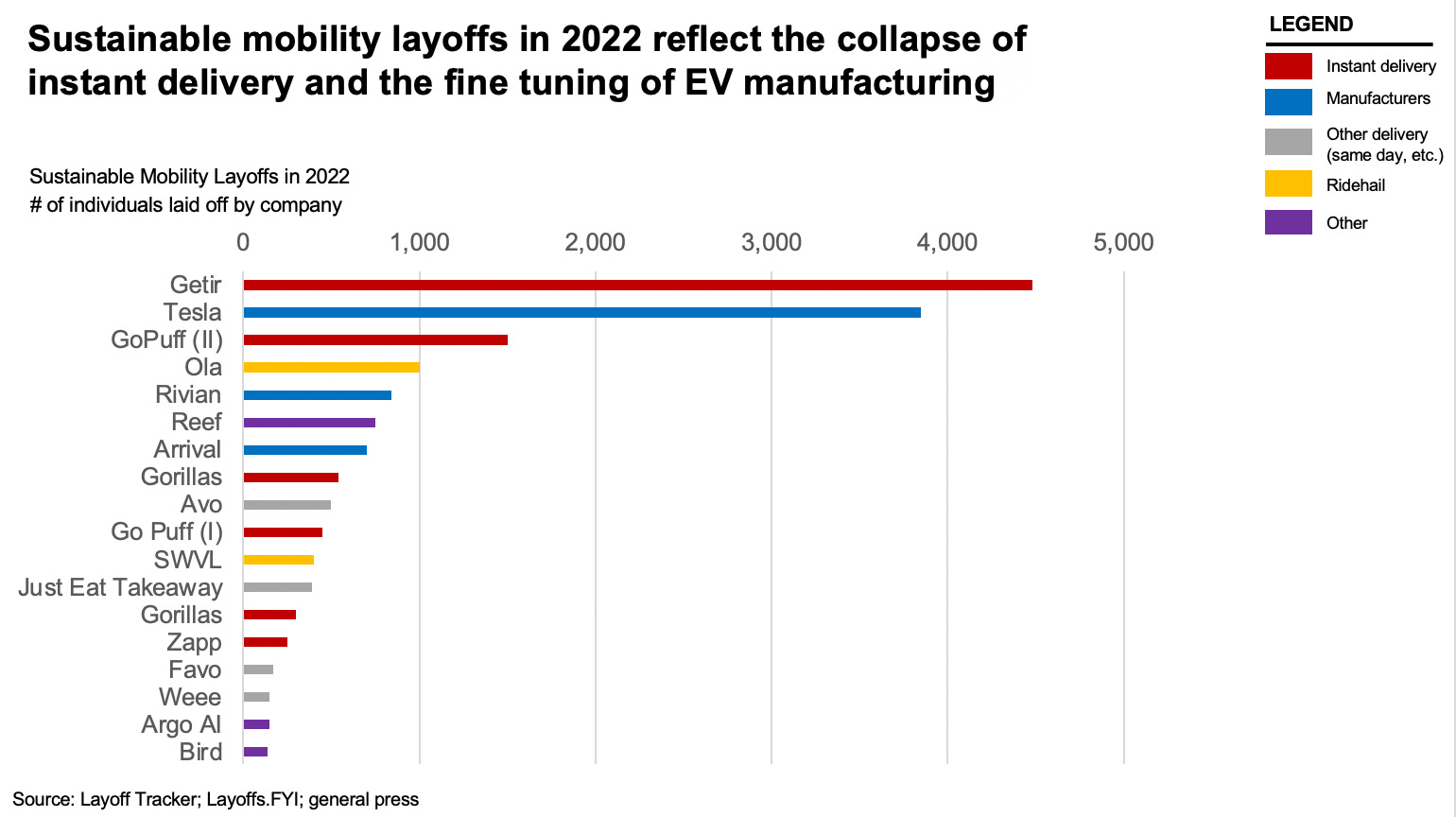

DEEP DIVE: Tracking the layoffs in sustainable mobility

Two weeks ago, Bloomberg revealed that Ford would lay off up to 8,000 staff from the legacy (internal combustion engine) portion of the business to fund growth in EVs.

However, at the same time as Ford is trying to downsize its staff in the non-sustainable portion of its business, sustainable mobility is going through its own turbulence given the economic uncertainty and cooling investor environment. So what’s happened so far in terms of layoffs in sustainable mobility?

While the headlines may just focus on the large number of layoffs, the data reflects dramatically different situations by sub-sector.

Instant delivery (i.e., toothpaste or booze delivered to your door in 15 minutes) was never explicitly sustainable mobility, but to the degree a significant portion of those deliveries come by e-bike, or could be transitioned to e-bike in near future, it may be a GHG improvement over the status quo. Despite the massive investor enthusiasm over the last few years, the category never held economic logic, at least in developed markets where loaded labor plus vehicle costs can easily exceed $20-$30/hour. The category is dead on arrival for now.

For EV manufacturers, it’s a different story. Companies like Rivian and Tesla are manufacturing in real numbers and are struggling with supply chain shortages. Reducing some of their fixed costs as they focus on securing incremental volumes makes great sense.

But perhaps the most interesting aspect of sustainable mobility layoffs is what subsectors are missing. You won’t find EV charging, maritime decarbonization, aviation decarbonization, fleet management, or batteries on public layoff databases. That’s probably more a function of the timing of when those subsectors became fundable than their underlying business strength. While founders in these subsectors may lament today’s more disciplined funding environment, it will likely help them in the next few years avoid situations like the instant delivery implosion. Call it the benefit of fundraising in a more rational environment.