♟Su$tainable Mobility, Volume 25

This newsletter aims to separate the signal from the noise for making money in sustainable transportation: Electrification, mode shift, active and public transit, and mobility aggregation, across both people and goods movement.

This week features a Deep Dive on What SEC Climate Disclosures Might Mean for Sustainable Mobility.

Two notes from friends:

PodSnacks is one newsletter to stay on top of all the climate podcasts. PodSnacks summarizes recent climate podcast episodes — it's like CliffsNotes for podcasts. https://www.podsnacks.org to receive the free weekly newsletter.

Mobility Makers have recently launched the first-ever Mobility Makers Hub at WeWork Paris dedicated 100% to sustainable mobility. The goal of the Hub is to meet, work and network in a workspace dedicated to sustainable mobility and to bring together local industry professionals to create synergies and drive the entire sector forward.

STARTUP WATCH

🚙 Battle Approved Motors (Arizona, USA): EV utility terrain vehicles (UTVs)

🎟 BuuPass (Kenya): Mobility aggregator and payments platform

🗺 CēVē (Florida, USA): Smartphone app and cloud service that connects drivers to transportation infrastructure

🛴 Ride Beyond (Formerly Brooklyness) (New York, USA): Kick scooter subscription service

🗺 Save Biking (Italy): Consumer app with gamification for sustainable mobility choices

🚢 Seabound (UK): Carbon capture equipment for large cargo ships

💳 Spring Free EV (California, USA): Fintech for EV buyers (mileage purchase agreement)

🎟 Transtura (Nigeria): Mobility aggregator and payments platform

📦 Wings (Massachusetts, USA): Autonomous micro-fulfillment and distribution

🏪 Zeem Solutions (California, USA): Electric-truck depots-as-a-service

📦 Zero Emissions Services (Netherlands): All-in-one concept for emission-free inland shipping

QUICK HITS

💣 SEC proposes new rules for SPACs, potentially ending the safe harbor for projections. For a still-nascent market like cleantech, the ability to get to public markets via SPAC based on future-looking projections (e.g., EV car sales market growth) was a key advantage versus the traditional IPO, which offers no such future-looking projections. If the SEC proceeds with this, it makes the SPAC a non-starter for many companies.

🚕 Uber will let you book a taxi in NYC, following similar moves in overseas markets. Faced with driver shortages and the desire to become a mobility aggregator, this makes sense.

🤝 MIT makes the case for cities coordinating between ride-hail operators. There is indeed an emissions and congestion penalty for a city when a Lyft-loyal consumer hails their ride from a Lyft driver 4 miles away while the nearest Uber driver is 3 blocks away. Whether cities do anything with this information is another question.

📉Shift, the used car marketplace, acquires Fair for $15M. Fair raised over $2B in debt and equity to try to bring auto subscriptions to scale, a reminder of how cash-intensive it can be to pioneer new sales and car usage models.

🚄Washington State is moving forward with a high-speed rail plan to link Portland, Seattle & Vancouver. It’s still unclear whether high-speed rail will ever scale in the US, even if its role is secure in Europe and East Asia and growing in North Africa.

⚔️ US President Biden invokes Defense Production Act to spur the domestic battery economy. The US is woefully behind China and clearly lagging Europe in the battery race, so invoking a whole-of-government approach is overdue.

⚛️ Scientists at Korea's Institute for Basic Science (IBS) proposed “quantum charging” for EVs. While the goal is to charge an EV at the same rate as a gas-powered car, it’s important to keep in mind how different the usage and fueling experience inherently is. For those with charging at home, leaving the house with full range on an EV is the norm.

⛽️ Porsche is getting into synthetic fuels. Synthetic fuels have a poor record of being sustainable.

🛥 California imposes new air quality rules on harbor boats. Unlike hard-to-decarbonize ocean vessels, zero-emissions small boats are a technical and commercial reality.

🚲 Boston is launching an e-cargo bike pilot focused on small businesses. Last-mile delivery by e-cargo bike is a winning formula so long as the density is sufficient.

🏪 Instacart will build micro-warehouses, aiming to better compete with both Amazon and the instant delivery crow. This comes as Instacart slashed its own (409a) valuation by 40%.

🚸 LA residents are going rogue to paint crosswalks. It’s rare that residents of any city voluntarily do unauthorized manual labor on behalf of city services.

DEEP DIVE: WHAT SEC CLIMATE DISCLOSURES MIGHT MEAN FOR SUSTAINABLE MOBILITY

At long last, the US Securities & Exchange Commission (SEC) has proposed climate disclosure rules.

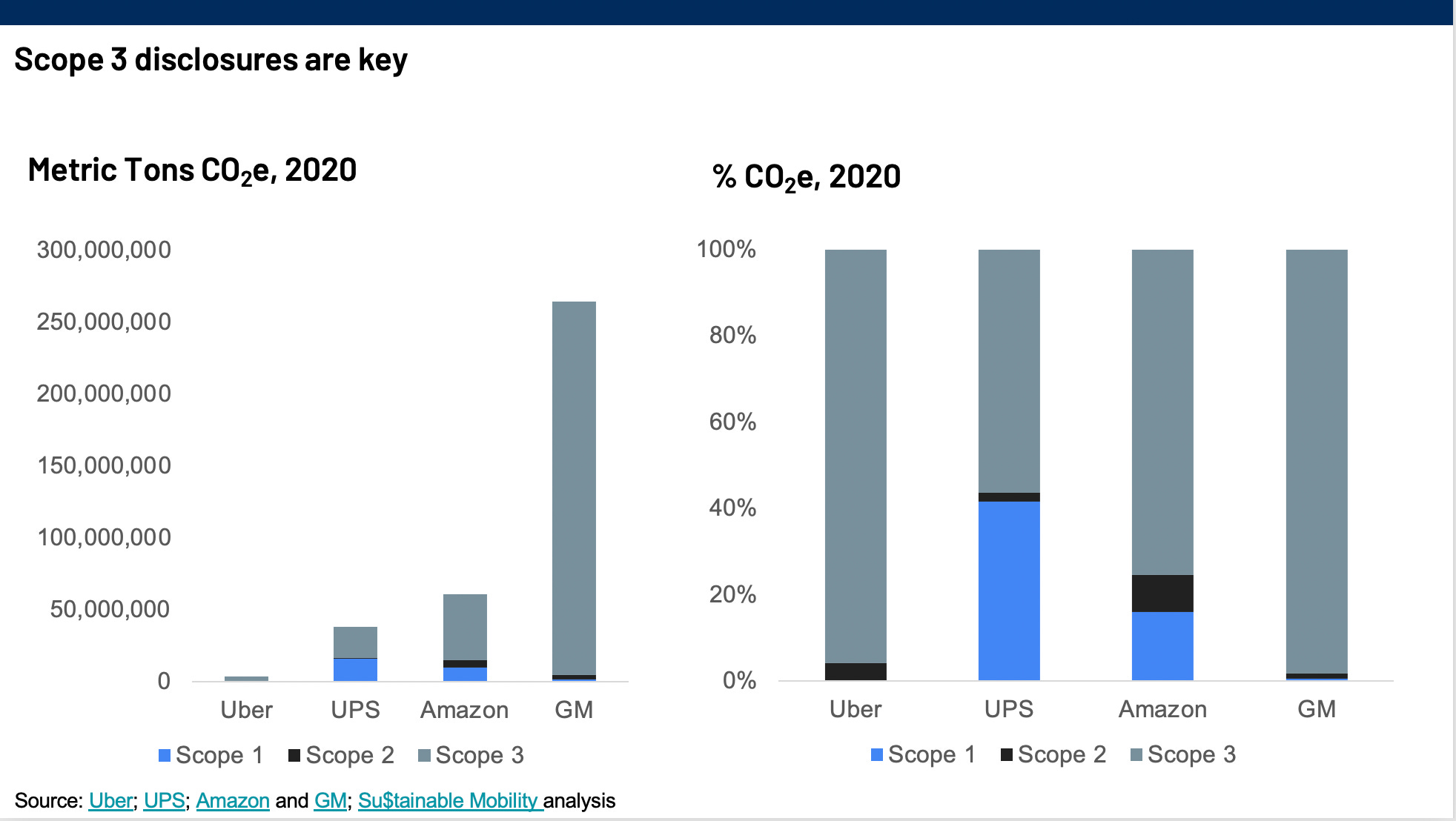

As the SEC undertakes a comment period, keep an eye on the scope 3 requirements. The current wording states “a registrant would be required to disclose GHG emissions from upstream and downstream activities in its value chain (Scope 3), if material or if the registrant has set a GHG emissions target or goal that includes Scope 3 emissions.” How this scope 3 rule is implemented has a vital impact across all transportation sectors, including mobility providers, logistics providers and vehicle manufacturers.

For emissions relating to Uber’s business model, scope 1 is stationary emissions, scope 2 is location-based electricity, and scope 3 includes the usage of the Uber products (e.g, drivers performing rides). Consistent, standardized Scope 3 reporting by Uber and Lyft will allow investors to see what both are really doing to decarbonize their drivers’ fleets versus how they would prefer to spin the story.

For UPS, DHL, FedEx, and Amazon, the scope 1, 2, and 3 distinctions may be even more crucial.

UPS operates its own fleet of last-mile trucks, so it’s not surprising that scope 1 emissions were 41% of its total CO2e emissions. Amazon, however, fulfills a large portion of last-mile delivery via its own network of Amazon flex gig workers and Delivery Service Partners, quasi-franchisees with up to 40 vans.

UPS and Amazon are fundamentally doing the same thing in last-mile delivery, but whether and how scope 3 gets reported makes all the difference.

For auto manufacturers, the role of third-party auditors may be vital. Thus far, climate disclosures by corporations have been self-certified or approved by organizations with less on the line than what the SEC would likely demand.

In the US, a 10-K annual report provides a comprehensive overview of the company's business and financial condition. The cornerstone of the 10-K is the auditor’s report certifying that the contents fairly present the company’s financial situation. The auditor's value is their reputation for integrity; getting it wrong can mean the downfall of the entire auditing firm (remember Arthur Anderson?).

Where this may get difficult for car companies is the degree to which auditors accept arguments about fuel efficiency for vehicles like plug-in hybrids and internal-combustion engine vehicles. There is a large discrepancy between government-approved lab testing protocols for fuel efficiency (eg, so-called “type-approvals”) and real-world emissions. The International Council on Clean Transportation (ICCT) claims that “PHEV fuel consumption and tail-pipe CO2 emissions in real-world driving, on average, are approximately two to four times higher than type-approval values.”

Keep an eye on this process; it’s a truly seismic development for sustainable mobility. As such, expect strong resistance from those who claim these requirements violate the scope of the SEC’s mandate.